Mortgage Application Template

Here’s an HTML formatted explanation of a mortgage application template, aiming for clarity and detail around key sections: “`html

Mortgage Application Template: A Detailed Overview

A mortgage application template serves as a standardized form used by lenders to gather comprehensive information from potential borrowers. This data is crucial for evaluating the applicant’s creditworthiness and determining the feasibility of granting a mortgage loan. While specific templates may vary slightly between lenders, they generally cover the same core areas. Understanding these areas will help you prepare a complete and accurate application, increasing your chances of approval.

Key Sections of a Mortgage Application Template

The following sections outline the most important elements typically found within a mortgage application.

1. Borrower Information

This section collects personal details about the applicant(s). Expect to provide:

- Full Legal Name(s): Including middle name or initial.

- Social Security Number(s): Required for credit report verification.

- Date(s) of Birth: Used for identification and age verification.

- Current Address: Including street address, city, state, and zip code.

- Previous Address(es): If you’ve lived at your current address for less than two years.

- Phone Number(s): Both home and mobile numbers are often requested.

- Email Address: For communication and document delivery.

- Marital Status: Affects property ownership and potential co-borrower requirements.

- Number of Dependents: Can influence debt-to-income ratio calculations.

2. Employment Information

Lenders need to verify your employment history and income stability. This section usually includes:

- Current Employer’s Name and Address: Including phone number.

- Your Position/Title: Within the company.

- Length of Employment: How long you’ve worked at your current job.

- Gross Monthly Income: Before taxes and deductions.

- Previous Employer Information: If you’ve been at your current job for less than two years.

- Documentation: Expect to provide pay stubs, W-2 forms, and potentially tax returns to verify employment and income. Self-employed individuals will require additional documentation, such as profit and loss statements and business tax returns.

3. Income and Assets

This section details all sources of income and any assets you possess that can support the mortgage. This includes:

- Salary/Wages: As detailed in the employment section.

- Other Income: Including bonuses, commissions, alimony, child support, investment income, rental income, Social Security benefits, or pension income. You will need to provide supporting documentation for each source.

- Bank Accounts: Checking, savings, and money market accounts. Provide account numbers and balances.

- Retirement Accounts: 401(k)s, IRAs, and other retirement savings. Provide account numbers and balances.

- Investment Accounts: Stocks, bonds, mutual funds, and other investments. Provide account numbers and balances.

- Real Estate Holdings: If you own other properties, provide addresses, market values, mortgage balances, and rental income (if applicable).

- Other Assets: Such as life insurance policies with cash value or valuable personal property.

4. Liabilities

This section lists all your outstanding debts and financial obligations, which directly impact your debt-to-income ratio.

- Credit Card Debt: List each card, the outstanding balance, and the minimum monthly payment.

- Student Loans: List each loan, the outstanding balance, and the monthly payment.

- Auto Loans: List each loan, the outstanding balance, and the monthly payment.

- Other Loans: Personal loans, installment loans, etc. List each loan, the outstanding balance, and the monthly payment.

- Alimony/Child Support Payments: If applicable, list the monthly payment amount.

- Other Debts: Any other financial obligations that are not listed above.

5. Property Information

This section focuses on the property you intend to purchase or refinance.

- Property Address: Including street address, city, state, and zip code.

- Property Type: Single-family home, condo, townhome, etc.

- Purchase Price (if purchasing): Or estimated market value (if refinancing).

- Loan Amount: The amount you’re requesting to borrow.

- Down Payment Amount: And source of the down payment (e.g., savings, gift).

- Intended Use: Primary residence, secondary residence, or investment property.

- Year Built: Of the property.

6. Declarations

This section typically includes a series of yes/no questions regarding your financial history, such as:

- Have you ever declared bankruptcy?

- Are you currently involved in any lawsuits?

- Have you ever had a property foreclosed upon?

- Are you delinquent on any federal debt?

Be honest and thorough in answering these questions, as any discrepancies can raise red flags. You may need to provide explanations for any affirmative answers.

7. Acknowledgements and Signatures

This section confirms that you have read and understand the terms of the application and that the information you provided is accurate to the best of your knowledge. You and any co-borrowers will need to sign and date the application.

Tips for Completing a Mortgage Application

- Be Honest and Accurate: Provide truthful and complete information. Misrepresentation can lead to denial or even legal repercussions.

- Gather Documentation: Collect all necessary documents beforehand, such as pay stubs, W-2s, bank statements, and tax returns.

- Review Carefully: Proofread the application for errors before submitting it.

- Ask Questions: Don’t hesitate to ask the lender for clarification on any unclear sections.

- Work with a Mortgage Professional: Consider working with a mortgage broker who can guide you through the application process and help you find the best loan options.

By understanding the different sections of a mortgage application template and preparing accordingly, you can streamline the process and improve your chances of securing a mortgage loan that meets your needs.

“`

390×450 mortgage application templates word excel format from www.template.net

390×450 mortgage application templates word excel format from www.template.net  530×749 fillable mortgage application form printable from www.formsbank.com

530×749 fillable mortgage application form printable from www.formsbank.com  530×749 mortgage application form printable from www.formsbank.com

530×749 mortgage application form printable from www.formsbank.com  600×730 mortgage application template hq printable documents from whoamuu.blogspot.com

600×730 mortgage application template hq printable documents from whoamuu.blogspot.com  800×1035 mortgage applicationindiana legal forms from indianavirtuallaw.com

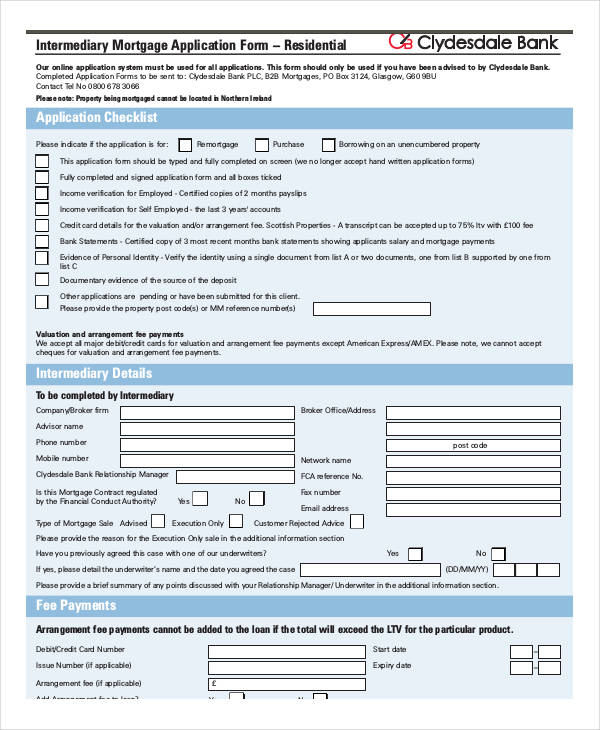

800×1035 mortgage applicationindiana legal forms from indianavirtuallaw.com  1275×1650 mortgage application from blog.thewestlaketeam.com

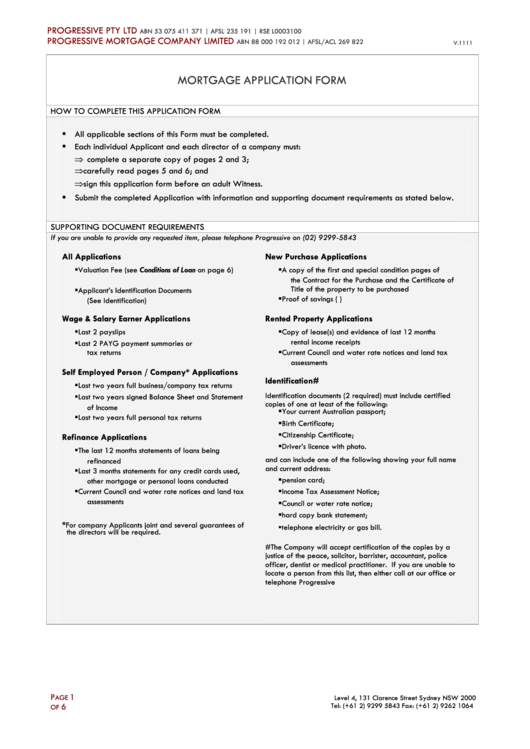

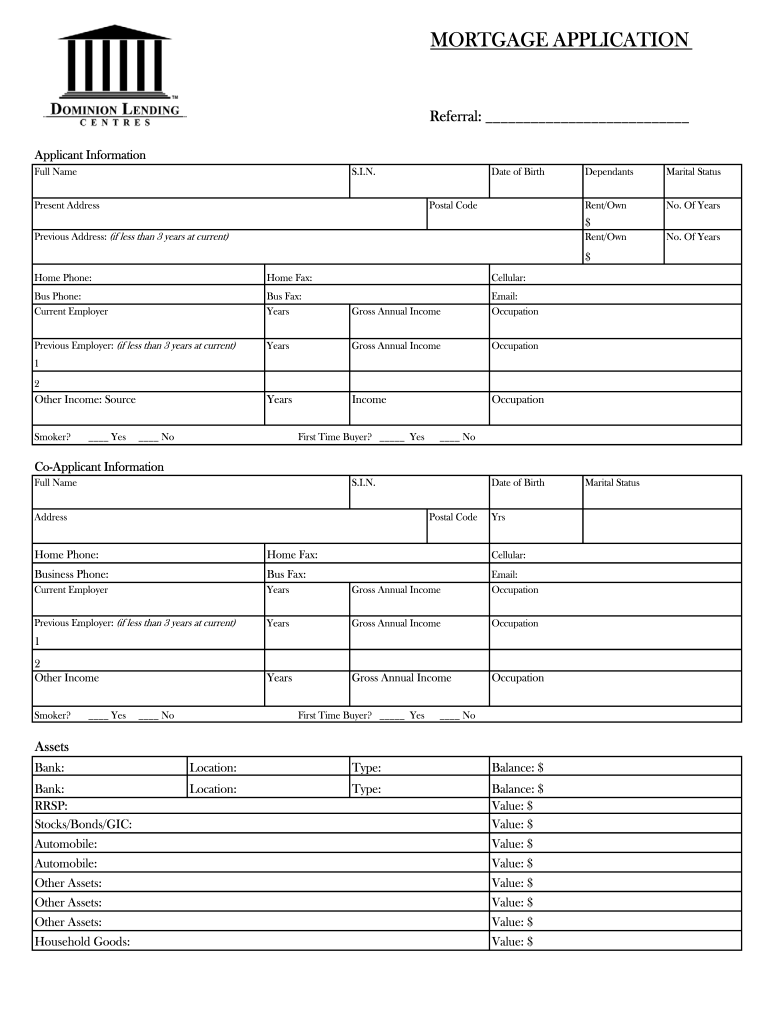

1275×1650 mortgage application from blog.thewestlaketeam.com  770×1024 mortgage loan application form fill printable fillable from dominion-lending-mortgage-application.pdffiller.com

770×1024 mortgage loan application form fill printable fillable from dominion-lending-mortgage-application.pdffiller.com